Traditional finance keeps a large share of the difference between what borrowers pay and what lenders earn. On Skew, you earn more.

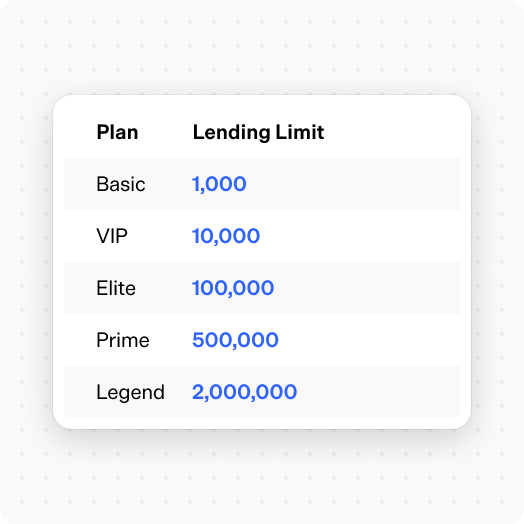

Your membership plan determines your lending limit.

Members fund real people and businesses. Borrowers and lenders connect directly.

Skew connects you to vetted borrowers on a fully regulated platform. You know exactly where your money goes.

Set your lending terms and manage everything from the dashboard. Your money, your rules.

Your lending rate is agreed upfront so you always know what you'll earn. No market volatility. No variable rates.

Most people finish in a few minutes. You’re always in control.

What is Member lending?

Member lending is the core feature of the Skew platform. As a Skew member, you have exclusive access to fund vetted projects and businesses you believe in. Review borrower profiles, understand how the funds will be used, and choose where to lend, with a fixed APR and term agreed before you commit.

Interest is credited to your account daily and can be claimed at any time. At the end of each loan, your funds need to be claimed back before they become available for a new loan.

This is not a savings account. It is a member-based direct lending arrangement between you and a borrower, facilitated by Skew. The terms are transparent, the rate is fixed, and the control stays with you.

How does lending work on Skew?

Skew lists member lending opportunities from vetted borrowers. Each opportunity includes a borrower profile, the funding goal, the APR, and the lending term so you can review the details before deciding to participate.

If you choose to lend, you select the amount you would like to contribute, starting from $5. Your funds are then reserved during the subscription period while other members decide whether to participate.

The loan starts automatically when either the full funding goal is reached or the minimum funding requirement is met at the end of the subscription period. Once the loan starts, your lending term begins and interest starts accruing daily.

Is the APR quoted as annual or monthly?

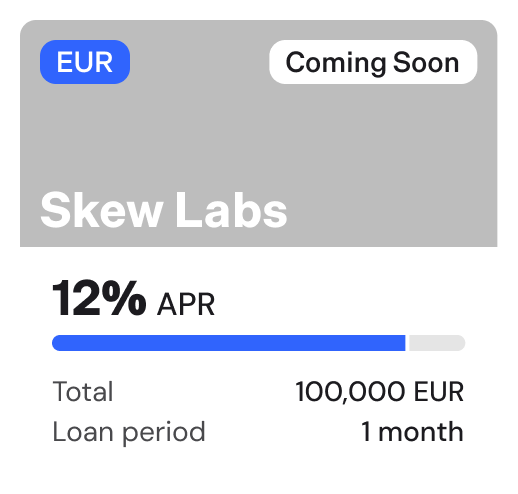

The APR is an annual rate and stays fixed for the full lending term. At 12% APR, a €10,000 lending balance earns approximately €3.29 per day.

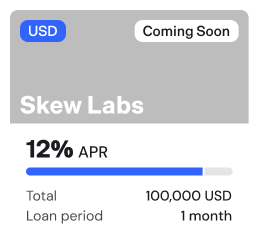

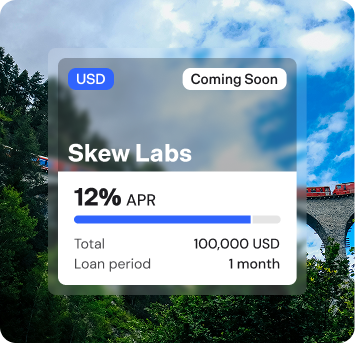

The APR is an annual rate and stays fixed for the full lending term. At 12% APR, a $10,000 lending balance earns approximately $3.29 per day.

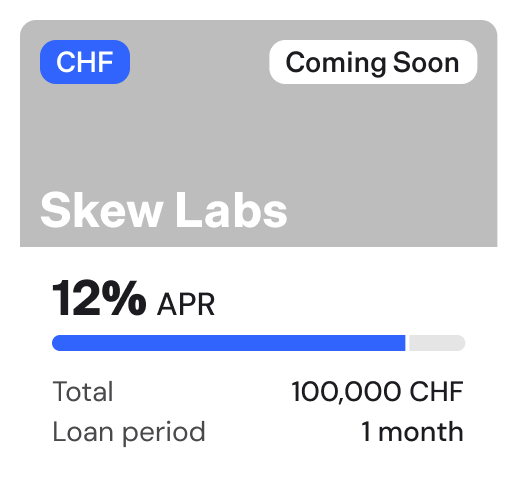

The APR is an annual rate and stays fixed for the full lending term. At 12% APR, a CHF 10.000 lending balance earns approximately CHF 3.29 per day.

Can I withdraw my funds before the lending period ends?

No. Once your funds are committed to a lending opportunity, they are locked for the full lending term and cannot be withdrawn early.

Before lending, make sure you are comfortable leaving your funds committed for the entire lending period.

If needed, you may claim your available interest before the lending period ends, but a 20% penalty fee will be applied to the amount available to claim.

What happens if a borrower defaults?

Borrowers are reviewed before being listed on the platform, and lending limits may increase gradually based on repayment performance and lending history. Any collateral provided is disclosed to members before funds are committed.

If a borrower defaults, Skew will take all reasonable steps available to recover funds on behalf of members. This may include enforcing loan agreements, pursuing legal remedies, and liquidating any collateral provided by the borrower.

However, member lending involves risk. If recovery efforts are unsuccessful or only partially successful, members may experience a loss on the affected lending position. There is no guarantee fund or insurance program that covers borrower defaults.

At launch, the only available borrower is Skew Labs, through a promotional lending opportunity offered by the company behind the platform, so members know exactly who they are lending to. As additional projects and businesses are added, each borrower will be vetted before being listed, and all lending terms and collateral arrangements will be fully disclosed.

Is Skew regulated?

Yes. Skew Labs SA operates under Swiss financial regulation. This means the platform is subject to Swiss anti-money laundering law and financial services standards. Regulation does not eliminate lending risk, but it means the platform operates within a defined legal framework with obligations to its members.

Follow and subscribe to our channels.

Proudly Swiss.

From Lugano, Switzerland.

© 2026 Skew, All Rights Reserved.

Skew is powered by Skew Labs SA, a Swiss company operating the Skew brand globally whose registered office is Via F. Pelli 13, Lugano 6900, Switzerland. Skew Labs SA is affiliated to SO-FIT as a financial intermediary within the meaning of article 2 para. 3 of the Anti-Money Laundering Act (AMLA). SO-FIT is a self-regulatory organization recognized by the Swiss Federal Financial Markets Supervisory Authority (FINMA). Availability of the Skew services depends on your location, which may affect your rights and protections; therefore, please read the terms and conditions that apply to you carefully. Tax may be payable on profits. You access Skew services on your own initiative and without solicitation.